See the ‘Market Data’ post.

Good evening,

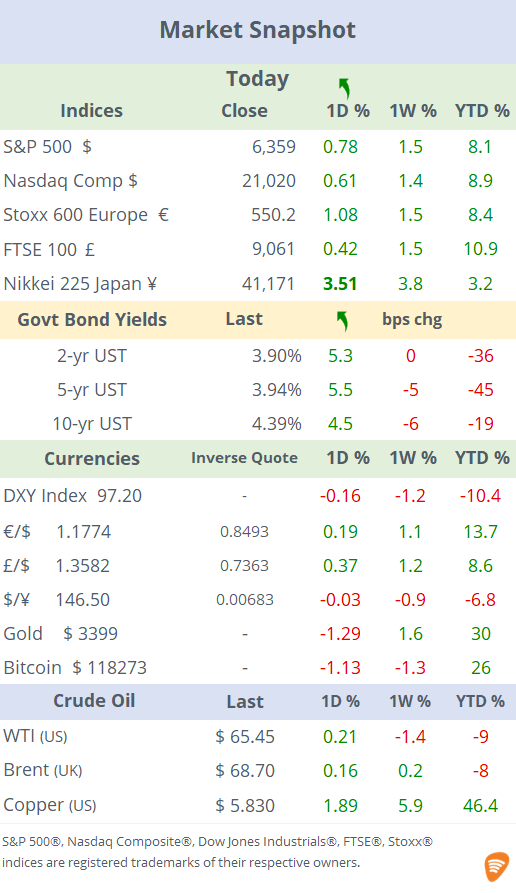

Markets focused on trade developments and corporate earnings, as Trump finalised a deal with Japan, Brussels moved closer to a similar agreement, and several blue-chips posted strong results ahead of Tesla and Alphabet’s reports after the close. Global equities rallied, the S&P 500 closed at a new record high, Tokyo’s Nikkei 225 gained 3.5% today to a one-year high, US Treasury yields rose ~5bp, and the $ was little changed.

On the tariff front, the White House signed a historic trade deal with Japan late Tuesday. Under the deal, US importers will face a 15% 'reciprocal' tariff on Japanese exports. Crucially for Japan, this rate will also apply to automobiles and car parts, giving it an edge over other major car-exporting nations, which have been subject to a 25% tariff on auto-related exports since April. The EU is close to finalising a similar deal, though it has not yet been confirmed.

Earnings: large-caps reporting before the open, GE Vernova, Thermo Fisher and CME Group, beat estimates and were highly upbeat, with energy giant GEV (mcap $171bn) delivering a standout performance and upgrading its full-year guidance. Shares rallied 14.6% to a fresh record and accumulated a 91% gain YTD. Thermo Fisher (mcap $176bn) also upgraded its outlook and shares advanced 9% but remain 10% weaker this year. Texas Instruments (mcap $169bn) reported yesterday after the close, and shares plunged 13% today on poor guidance despite beating top and bottom estimates.

After the close, Alphabet beat top ($96bn, +14% YoY) and bottom ($28bn, +22% YoY, $2.31/share) estimates. Positive on growth and AI & Cloud strength but slightly dampened by aggressive capex outlook (+$10bn), and investors reacted nervously in extended trading with shares falling ~1%.

Tesla missed both revenue ($22.5bn, -12% YoY) and earnings ($1.4bn, -23% YoY) estimates. The stock held steady in extended trading after saying its "more affordable" model was still scheduled for production in H2’25. Tesla delivered 384k vehicles globally in Q2, a 13.5% drop YoY. (CNN)

Economic data took a back seat today, and there were no central bank policy meetings to highlight.

Corporate deals: Iberdrola (mcap €94bn), Europe's largest utility, raised €5bn via an accelerated share bookbuild, the biggest in a decade in Spain, to finance investments in power grids in the UK and US. It was priced at €15.1, and shares fell 4.7%. (Reuters)

In Italian banking, UniCredit has withdrawn its ~€14bn all-share takeover bid for rival Banco BPM after opposition from Meloni’s government, which prefers a merger between BPM and Monte dei Paschi di Siena. BPM shares fell 2.5%. (Bloomberg)

IPO: NIQ Global Intelligence, a consumer insight and data company backed by private equity firms KKR and Advent International, raised $1.05bn, was priced at $21 on its NYSE listing at a market value of $6.3bn. Shares declined over 7% on their debut today. (NIQ)

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.