See the ‘Market Data’ post.

Good evening,

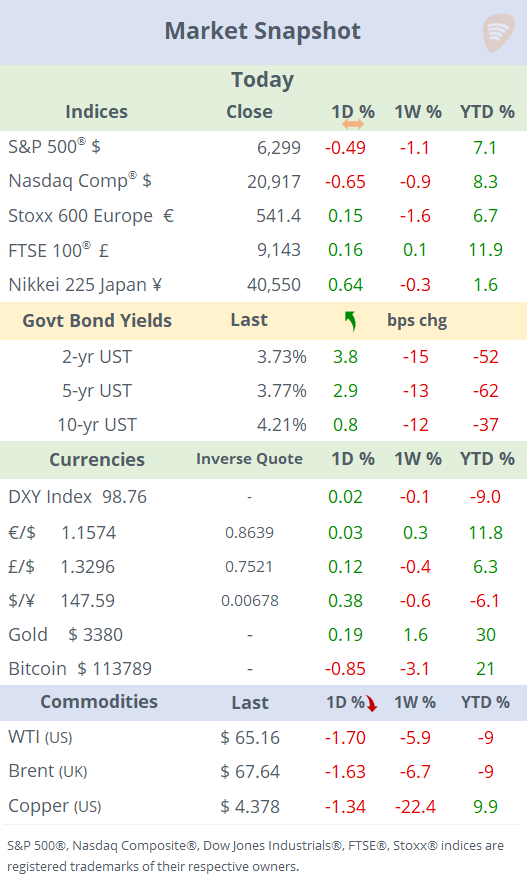

Markets saw a relatively uneventful Tuesday compared with the last few days, with limited headlines to shape momentum. Mixed-to-weak economic data and renewed tariff headlines weighed on markets, pulling major US indices lower following Monday’s rally. Leading stock benchmarks finished down ~0.5%, the $ index continues to trade sideways, while Treasury yields rose marginally (an auction of 3-yr notes attracted soft demand).

Crude oil slid over 1.5% again today as OPEC+ ramped up supply on Sunday, expectations for demand softened, and markets digested recessionary risks, continuing a multi-day downward trend with Brent down by nearly 7% in the past week to $67.6.

Trump announced plans to “substantially raise” tariffs on Indian imports beyond the existing 25%, citing India’s continued purchase and resale of Russian oil as a means of funding the war in Ukraine. He also intends to introduce tariffs on semiconductors and pharmaceuticals "within the next week or so," noting that drug import taxes could ultimately reach 250%.

It was a quieter day for earnings releases with chip maker AMD (mcap $282bn) and biotech Amgen (mcap $161bn) reporting after the close. Both beat revenue estimates, but AMD missed on profits (despite the +230% YoY jump), and shares dropped over 4% on extended trading hours, although it lifted guidance, while Amgen traded marginally weaker. Caterpillar also missed earnings forecast before the open, but shares recovered from an initial drop to end almost unchanged.

Notable mover: the 21% drop in Vertex Pharma (mcap $96bn) shares, despite yesterday’s robust earnings beat, is tied to pipeline setbacks. Its experimental painkiller failed a mid-stage trial. Stock is down 7% YTD.

Reports tomorrow: Novo Nordisk, McDonald's, Uber, Shopify and Airbnb.

Economics: The final readings for July’s Services PMI surveys were the main data updates. The US ISM (Institute for Supply Management), which surveys large companies, suggested a slowdown in activity to 50.1 points, well below estimates, while the S&P Global measure, which surveys a broader base and includes SMEs, showed solid growth at 55.7 points with increasing demand and hiring.

Germany is showing early signs of recovery (50.6), and China’s services sector signalled robust strength and accelerating growth, outperforming both manufacturing and expectations (52.6).

Deals: Global corporate deals have hit $2.6tn, the strongest start to a year since the 2021 pandemic-era peak, as corporate boards pursue growth and booming AI activity offsets uncertainty from tariffs.

Today’s update: British scientific instruments maker Spectris Plc (mcap £4.1bn), became the target of two large private equity firms. After recommending a takeover bid from Advent International last week, it is now accepting an improved bid from KKR for an equity value of £4.2bn. The stock barely moved today, closing at £41.10, slightly below KKR’s £41.75 bid.

In the US utilities sector, Duke Energy (mcap $97bn) sold ~20% of its Florida business to Canadian investment manager Brookfield for $6bn in cash.

Business news: BP (mcap £64bn) announced its biggest oil and gas discovery in 25 years in the Santos Basin off the coast of Brazil. BP reported strong results today, beating top and bottom estimates, raised its dividend by 4%, announced a $750mn share buyback and 6,200 job cuts. Shares added ~3% today (+6% YTD).

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.